What’s Worked, What Hasn’t, and What’s Different From the US Mortgage System

When Mortgages Get Medieval: A Global Tour of Super-Long Loans

Let’s face it, your average 30-year fixed-rate mortgage is a bit, well, boring. It’s the dependable sedan of financial products—gets you there safely, but does it do the work that we need it to do? That is, are houses within reach for enough buyers? It’s not a question that we can get answered completely, but it’s worth considering what else is out there.

If you’ve read my blog over here or follow my daily posts on LinkedIn, not to mention my book(!), you know that I often dive into the psychology of homebuying. And like any other part of homeownership, a mortgage isn’t just paperwork tied to your bank account; it is the gatekeeper, tied to your deepest desires and sense of belonging. So, what happens when we throw caution to the wind and extend that pledge beyond our lifetimes? We get a hilarious, terrifying, and surprisingly insightful journey through global real estate history. And we get more than we bargained for as it relates to psychology, too.

Why think about this now? There are some pretty funky ideas getting floated in the US today, things that we haven’t seen. And they sound so crazy that we wonder if these ideas are out of the clear blue sky. For better or worse, they have been tried before and failed, are currently in use, or simply have never made it to our shores. With that in mind, grab your finest monocle and a balance sheet, because we’re examining the super-long mortgage.

Switzerland: The Heirloom Mortgage (The 100-Year Swiss Version)

In the world of mortgages, Swiss banks aren’t just in a different league; they’re playing a different sport, possibly while wearing lederhosen.

Imagine securing a loan that your great-great-grandchildren will still be dutifully chipping away at. That’s the 100-year Swiss mortgage. It’s the financial equivalent of a family heirloom—a handsome burden passed down through generations, along with Grandma’s passive-aggressive recipe book.

- The Pitch: Don’t worry about paying down the principal, ever! These were often interest-only loans where the principal was never the main attraction. The real goal was allowing the borrower (or, more likely, their heirs) to perpetually offset their mortgage interest against taxable income.

- The Vibe: Utterly practical and predictable, just like the Swiss. They assume generational wealth transfer, continuous employment, and a functioning financial market for the next century. It’s a system built on the assumption that the future will look exactly like a pristine Alpine village—static, beautiful, and slightly boring.

- The Joke: You finally close on your house, but the amortization schedule is signed by your great-grandson’s lawyer. The monthly payments are low, but the emotional commitment is Biblical. It elevates your home from a mere asset to a dynastic curse, ensuring your family remains financially intertwined for a century.

- A Financial Note: Requiring a 20% downpayment, it’s broken into a 65% LTV mortgage, and a 15% amortizing component, which must be paid before the homeowner retires. It doesn’t put all of the burden on future generations, but certainly burdens them!

How would this make you feel? What if you want to move? This kind of mortgage reflects a view of home that feels utterly foreign to the US conception today. Though, as we live longer and longer, the weird short stories of Kurt Vonnegut weigh on my mind. Specifically, the idea that we could eventually see generations all living together, forever, described hilariously in his 1968 Welcome to the Monkey House.

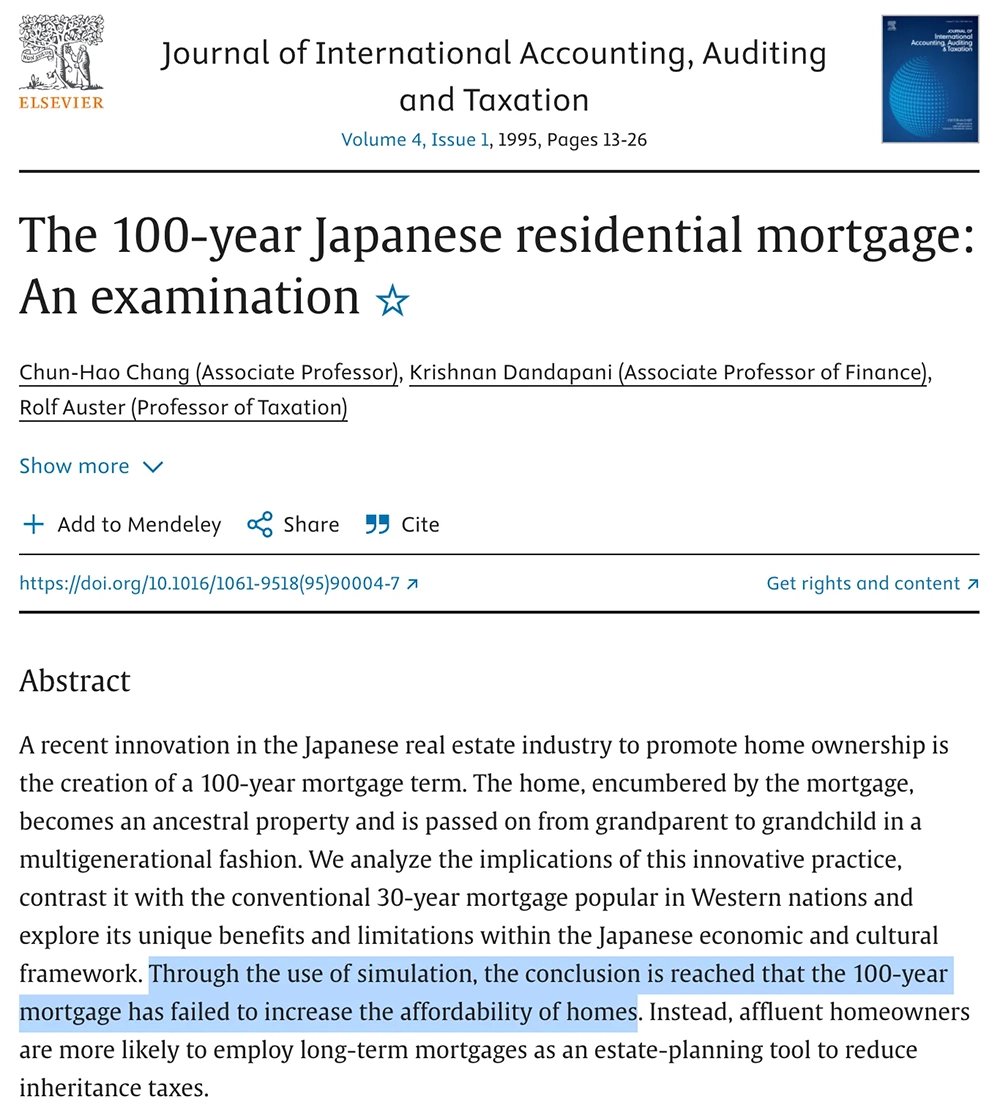

Japan: The 1990s Bubble Mortgage

Now, let’s step into the late 1980s and 1990s Japan, where things were decidedly less sensible. This is a tale of ambition meeting a terrifying, runaway asset bubble.

As the Japanese economic miracle reached peak fervor, 100-year mortgages appeared. These loans were often structured so that the final principal payment was passed to the grandchildren, making them feel like a multi-generational commitment, though they were often more complex, joint arrangements.

- The Pitch: The property value is only going to go up, forever. This was the siren call of a market that believed it had defied gravity. Mortgages were based on inflated property valuations that, let’s just say, did not age well.

- The Vibe: Fast, frantic, and reckless. It wasn’t about generational tax planning; it was about getting your slice of the perpetually rising market now, leveraging the perceived endless growth.

- The Aftermath: The Japanese asset price bubble burst spectacularly in the early 1990s. The value of these homes often plummeted, leaving the “debt-samurai” and their bewildered heirs to service debt far exceeding the actual value of the property.

Talk about financial turbulence! It was a painful lesson that no mortgage term, however long, can save you from a catastrophic market collapse. This is not viable for anyone. I, for one, am glad someone tried it first.

The USA Today: The Flexible Future

In America, we are currently flirting with the idea of longer loans. Why? Because the current market climate is “uncooperative”: housing prices are high, inventory is low, and interest rates are whipsawing. Buyers, those emotional heroes we real estate agents coach, are stressed out and looking for any edge they can get.

Today’s proposed 50-year mortgages and new portable mortgages (where you can take your existing low rate to a new property) are the industry’s answer to this market friction:

- The 50-Year Fix: This is the most straightforward heir to the long-loan dynasty. By stretching the amortization schedule from 30 to 50 years, you lower the monthly payment. It’s a nod to the fact that for many, the cost of entry is simply too high. It tries to answer the fear of unaffordability by making the monthly payment more digestible so that more young buyers enter the market.

- The Portable Perk: This is the truly innovative—dare I say magnetic—concept. It detaches the buyer from the crippling worry of a new, high-rate mortgage when they sell and move. It counters the feeling that those in 2-3% mortgages are forever trapped in their larger homes. But what does it do to help new buyers?

I can’t imagine that the portable mortgage is a viable option, anyway. Banks, for obvious reasons, are unlikely to agree to it. It would tie up assets and would depress their long-term prospects for revenue, to say the least! And regarding the 50-year mortgage, it doesn’t do enough today to be viable, either. The slightly-lower monthly cost pales when compared to just doing an interest-only mortgage today, and rolling into a fixed-rate mortgage when rates drop.

The World Tries to Adjust for Rising Housing Values

In the end, whether it’s the generational commitment of the Swiss, the reckless enthusiasm of 1990s Japan, or the cautious affordability strategies of modern America, every long-term loan reveals a fundamental truth of real estate: home is important to our wellbeing. The goal isn’t the mortgage term, but enabling more people to have the moment they can finally say, it’s good to be home.

Scott Harris is a veteran real estate agent and the founder of boutique New York City real estate firm Magnetic, and the author of new book The Pursuit of Home: A Real Estate Guide to Achieving the American Dream (Matt Holt Books), available now. Pick up your own copy today!